My family’s relationship with home owning has been fairly typical for a white American household. My grandparents, on both sides of my family, were born during the baby boom following World War II and purchased homes during the bonanza of building America experienced during the 1950s. Even though they were blue-collar workers, they managed to go into retirement with savings and homes — an American Dream that many in my generation can only dream of. Homeownership was crucial in my grandparents’ financial strategies, freeing them from indefinite renting and giving them space and solid communities in which to raise children.

However, the economics of housing have shifted in the past 60 years. Capital markets appreciate at record rates, with the S&P 500 yielding an average yearly rate of 7%. Dollar for dollar, investing in a hedge fund or index fund is more profitable than investing in a house. At the same time, interest rates, homeowners’ insurance and Realtor fees are making homeownership increasingly costly. All of these factors have converged to tip the scales, and at least in the Twin Cities, renting is now more profitable than buying.

This may seem counterintuitive. The main factor at play is opportunity cost – what you give up in order to make an investment. Suppose Alice invests $300,000 into the stock market at a 7% annual return, and Bob invests $300,000 in a house with a 6% annual increase. In 10 years, Bob ends up with $537,254 and Alice with $590,145. We say that Bob pays an opportunity cost of $52,851 for his decision of investment.

Oftentimes, opportunity cost makes the cost of homeownership less optimal than renting and investing the difference. To make this effect concrete, I used the New York Times’ calculator to calculate savings and costs in various regions of the Twin Cities metro, given assumptions about investment performance and increase in property values. The calculator considers how much money you could have made by investing a down payment (and then paying for rent), versus going ahead and spending it on a house, condo or townhome.

The first comparison group is a renter in Minneapolis sharing an apartment with a partner or roommate, versus a homebuyer in Minnetonka (a representative higher-income suburb). Hypothetically, both begin with enough money to make a down payment. The city dweller decides to put that money into investments, and the suburbanite chooses to purchase a home. I assume a 7% rate of return on an investment, again, consistent with the 20-year S&P 500 average, and a 6.3% home appreciation rate, consistent with regional averages.

Median rent in Minneapolis comes out to $1,629, meaning $815 per person. Renting then costs $149,275 over 10 years — which is good, but significantly less than the $279,279 that purchasing a median home in Minnetonka would cost (factoring in opportunity cost, Realtor fees, maintenance, utilities). Altogether, the Minneapolitan saves over $100,000 compared with the Minnetonka resident. This can then be money spent on shopping sprees with friends, on vacations, on a cabin up north. The renter ends up with a life of more varied experiences, and with more equity to boot – a reversal of the classic situation.

Of course, living in the city comes with savings besides the pure rental yields. The largest benefits come from reduced utility bills and the ability to live car-free. AAA estimates that the cost of new-car ownership is over $1,000 per month. If the thrifty Minneapolitan throws this money instead into an investment portfolio, they could have an extra $175,000 by the end of 10 years! Furthermore, if the Minneapolis resident lives in an apartment, they will have dramatically lower heating and electric bills. After all, they only need to heat or cool a 1,000-square-foot apartment, which is also being climate controlled by its neighbors — not a massive, detached house. Data on utility costs is sparser, but it would seem a fair assumption that between utilities and cars, the Minneapolitan could save $200,000 over 10 years.

The picture is complicated when considering the math of working-class suburbs. Brooklyn Center, with a median home price of $290,000, is one of the cheapest metro-area suburbs in which to purchase a house. Even here, under the same assumptions we made for our Minnetonka example, renting still saves money. The Minneapolis renter would end up with an extra $64,000 – a more modest sum than in the Minnetonka case, but a large amount of money regardless. This amount of money could be life-changing. It could be the seed of a sizable retirement account, or a rainy-day fund in case of a recession or job loss.

The math of living in the Twin Cities themselves is similar to that of Brooklyn Center. St. Paul, for instance, has a median house price of $315,000; in Minneapolis the median price is $350,000. Right in the middle of the regional price range, the Twin Cities also offer a slightly less lucrative market. The annualized appreciation for a house in Minneapolis is 5.26% for January 2014 to May 2024, compared with 6.39% for the region as a whole. This can partially be explained by the events of 2020, with people perceiving the cities as more dangerous, and less desirable. Compound this with the higher property taxes (1.3% in Ramsey County versus 1.05% in Anoka County), and the situation of Twin Cities homebuyers is not good at all. The Minneapolitan renter would save $140,000 over 10 years, all things considered.

Of course, living in Minneapolis or St. Paul confers a massive financial opportunity —purchasing a home and taking on a roommate. Even charging just $800 per month could give the entrepreneurial homebuyer $115,000 over 10 years, which eclipses the $140,000 that renting would otherwise save in Minneapolis. It also gives the opportunity to live car-free or car-light, which has the massive benefits already discussed. Living in dense, walkable communities in Minneapolis pays off, no matter whether you buy or rent. Renting ultimately ekes out buying, but the savings of the city are there regardless if one rents or buys a home in Minneapolis or St. Paul.

Indeed, we have made this assumption throughout — that you diffuse costs of living with a roommate. However, our conclusions hold up even without it. The median one-bedroom apartment in Minneapolis goes for $1,100, meaning it saves $130,000 over buying a house in Minnetonka, $9,000 over Booklyn Center and $41,000 over Minneapolis.

Children, though, complicate the picture. They primarily need stability; moving homes and schools is a large burden and complicates their social lives. With the sorry state of renter protections, renting comes with instability, meaning it is likely that children in rental situations will face moving at some point. It follows that the $100,000 cost of a single-family home (or condo, for that matter) may make sense — for the mental and social health of your child, as well as the ease of mind that homeownership would bring to parents.

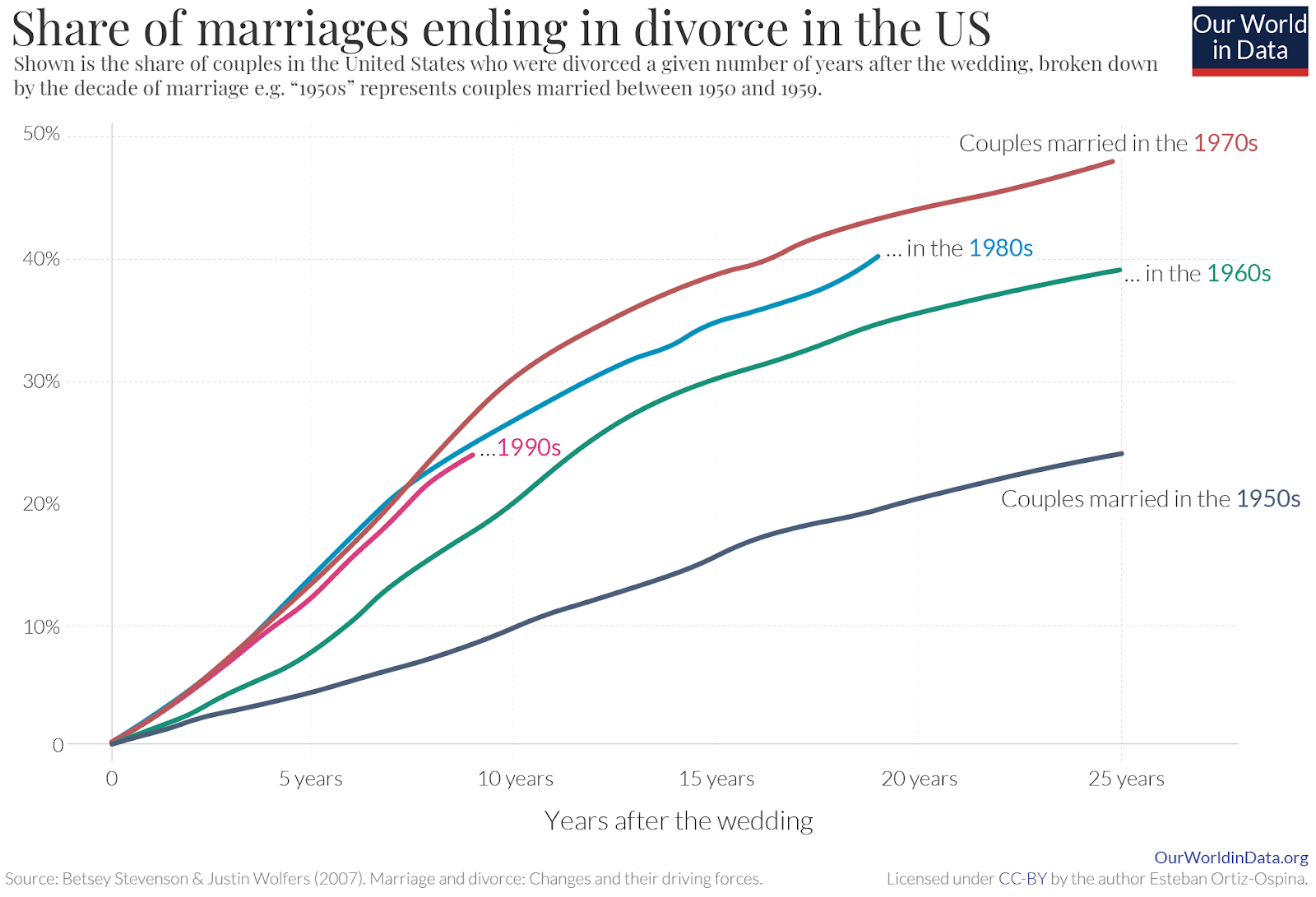

Even without children, though, homeownership makes more sense for couples. In this case, we assume that the couple pays for a two-bedroom that they occupy without a roommate. This would be far more expensive than a home, costing the couple $59,000 over 10 years versus homeownership in Minneapolis. Importantly, though, this does not take into account the probability of the relationship failing. Divorce rates for more recently married cohorts are around 25%. Should the relationship fail, the couple will be responsible for two separate housing situations — comparable to the scenarios offered prior. Relationships cannot be quantified, but it is difficult to pin a dollar amount on the risk of buying a home. It might be financially profitable to purchase a home for a couple, but the data suggest a bit more caution.

Thus far, the conversation has been fairly abstract. But it would be nice to think about what these dollar amount savings mean in context. Saving even just $50,000 over 10 years would be life changing for many people. Most Americans cannot afford a $500 surprise purchase, so to be able to sit comfortably on a year’s salary would lend a transformational level of security and peace of mind. Alternatively, $50,000 could buy a plethora of experiences. You could take 10 blowout overseas vacations, you could reinvest in your community and open a small business, you could buy a cabin up north. Or, in the end, you could decide to purchase a home anyway. In any case, you would be further ahead than the people who bought earlier.

Where you choose to live is an indication of what kind of community and lifestyle you want. Some people favor the quiet stability of suburbia, which is a completely valid preference. Paying the cost in driving time and expense, settling for less diversity and fewer activities, is worth it for some people, and we constantly make tradeoffs. Still, it is good to be fully aware of the tradeoffs you make and the factors that play into them. Ultimately, people’s preferences are their business, and no economic analysis can detract from that.

However, for 80 years we have been subject to a propaganda campaign about the virtues and fiscal wisdom of owning a home. This may have been true in the 1950s and ’60s, when government-backed loans and social programs opened up home ownership for a newly emergent middle class; my own white family benefited from the opportunities of this time, in a way that most Black Americans, for example, did not. But with a changing economy comes changing optimality, and owning a home no longer pays like it once did. Nowadays, it is better to invest in the future — into companies pushing us forward, into engineers creating new advances in technology and artificial intelligence, into new sources of power and climate resiliency. At least in the Minneapolis-St. Paul metro area, it is time to put the myth of the single-family home to rest.