Every time there’s a housing crisis — a wave of evictions, a spike in rent, a rash of foreclosures — we know what the political response looks like. Tenant organizers mobilize. City councils pass emergency ordinances. The moral vocabulary is already in place: people shouldn’t lose their homes because of a shock they didn’t cause.

That framework is right. It is also incomplete.

For tens of thousands of households across Minnesota, the crisis that finally breaks them won’t be a rent increase they can’t absorb. It will be a car payment they can’t make. A repossession notice on the vehicle that was getting them to the plant at 6 a.m. or to the suburbs for a low-wage retail job. We have a sophisticated political language for housing cost relief. We have almost nothing for transportation cost relief. That silence is costing people everything, right now, while we’re talking about other things.

The housing conversation draws the circle too small. Transportation is inside it — and for the households carrying the most debt, living farthest from frequent transit, working the jobs that start before the first bus runs, it may be the more urgent crisis of the two.

The Second Rent Nobody’s Talking About

Transportation is the second-largest household expense in America — behind housing, ahead of food and healthcare. A Brookings Institution analysis of the Twin Cities puts the average household at 17% of income spent on getting around, with low-income households well above that. In car-dependent neighborhoods — which is most of the metro — the numbers are starker: transportation can consume 25% of a household’s income, compared with 9% in walkable, bikeable, transit-rich areas. That 16-point gap doesn’t happen by accident. It’s the price of the built environment we chose — or had chosen for us.

AAA’s most recent “Your Driving Costs” study puts owning and operating a new vehicle at $11,577 per year. Nearly $965 a month, and that was calculated before the current gas price surge. For a two-income household running two vehicles, that’s over $23,000 before rent, food, or a single medical bill. For a family earning $60,000, that’s 40 cents of every dollar gone before the rest of life starts.

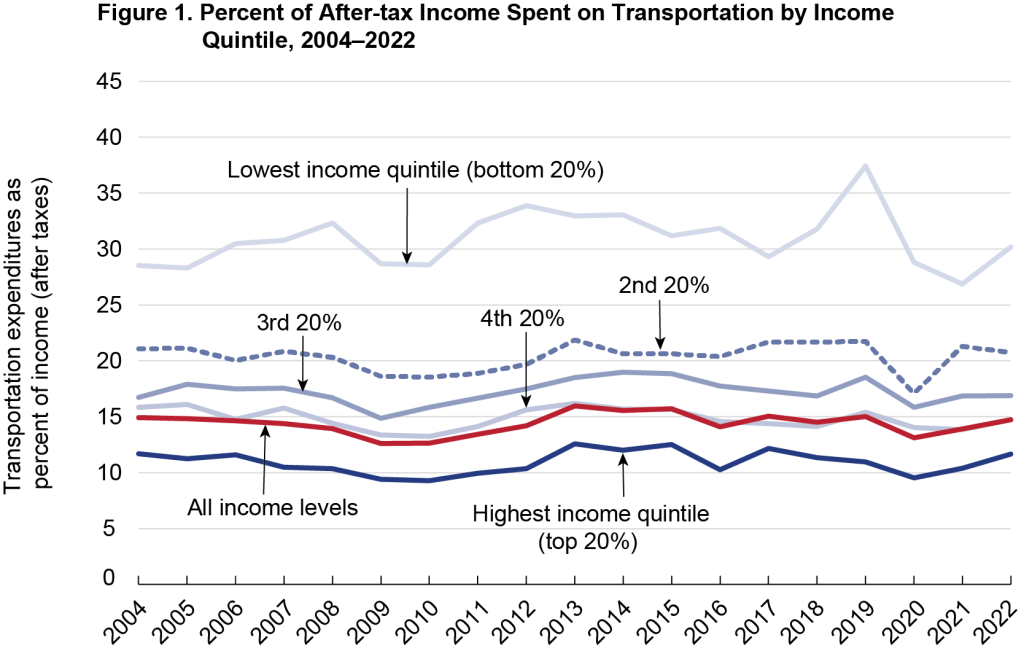

Housing advocates have long argued that no family should spend more than 30% of their income on rent. Here’s the number that doesn’t make it into those conversations: for households earning under $25,000, vehicle-owning households spent 38% of their after-tax income on transportation in the most recent federal data. Households without a vehicle spent 5%. Thirty-three percentage points less. That’s not a gap. That’s the difference between slow-motion financial collapse and something that might actually hold.

The combined housing-plus-transportation threshold that the Center for Neighborhood Technology uses to define affordability is 45%. In most of the Twin Cities metro, for a household with two cars and a modest rent, that threshold was already a memory before any of the current crises hit.

The Bubble That Was Always Going to Pop

As of Q4 2025, 5.2% of outstanding auto debt was at least 90 days past due, according to the New York Fed — approaching the all-time peak of 5.3% set during the financial crisis recovery in 2010. The difference is that the auto loan market is now roughly twice as large. More loans, higher balances, more households exposed. Average monthly payments hit a record $767 for new vehicles in Q4 2025. Nearly one in five loans tops $1,000 a month.

Among subprime borrowers — who, because of decades of discriminatory lending, disproportionately means Black and Latino families — the picture is worse. Subprime delinquencies hit 6.6% in early 2025, the highest since tracking began in 1994. Total delinquent auto loan balances exceeded $60 billion last year. With the Trump administration having sidelined the CFPB — the agency that would normally be investigating these issues — Sen. Elizabeth Warren launched a probe into the auto lending industry in February, sending letters to Chase Auto, GM Financial, Ally Financial, and a dozen other major players seeking data on repossession error rates and practices. She has since expanded that probe to include discriminatory lending to military service members. Neither investigation has produced federal action. There is no enforcement mechanism currently operating.

Think about how we respond to housing numbers like these. When mortgage delinquencies spiked in 2008, we got the Home Affordable Modification Program (HAMP). When pandemic income disruption hit renters in 2020, we got federal eviction moratoriums and $47 billion in emergency rental assistance — inadequate, slow, contested, but real. There is no equivalent for auto loans. No emergency forbearance program being debated in St. Paul. No moratorium on repossession for households experiencing documented income disruption. Just the repo man, and a bus schedule for a route that probably doesn’t reach the job — if there’s a bus, a protected bikeway, or any alternative at all.

This isn’t a coincidence. It reflects a settled political choice about which costs of living count and which ones are treated as personal problems. Housing is a right. Transportation is an individual consumer decision — even in a metro area where the built environment has made it physically impossible to live without a car.

Who Gets Hurt First, and Why

The racial geography of this crisis maps almost exactly onto the racial geography of the eviction crisis that housing advocates have been fighting for years. Rice University research found that Black and Hispanic borrowers face higher rejection rates and steeper costs than white borrowers with comparable credit profiles. Minority borrowers are 1.5% more likely to be denied. When they do get loans, they pay an average of 0.7% more in interest — roughly $410 more over the life of a typical loan, for the same car, the same credit, a different ZIP code and a different last name. $410 is a small number when viewed individually, but we are looking at a systematic problem that adds up to hundreds of thousands of dollars across a community. The Consumer Financial Protection Bureau found similar patterns, pointing to bias rather than creditworthiness as the driver.

North Minneapolis is a neighborhood where the conditions stack. Redlining kept homeownership — and the generational wealth that comes with it — out of reach for decades, which means thinner cushions, less margin, less room for a transmission to go out at the wrong time. The C Line along Penn and the routes along Broadway are real investments, and they matter. But they don’t run early enough or frequently enough to get someone to a 5 a.m. shift at a warehouse in Brooklyn Park or a hospital in the suburbs. So people take out the loan. Usually at the higher rate the data predicts. On a car that is simultaneously the household’s biggest liability and its only reliable path to a paycheck. When the car goes — and at current subprime delinquency rates, for a lot of these households it will — so does the job.

The communities most exposed to discriminatory auto lending are the same communities most exposed to redlining, exclusionary zoning, predatory mortgage lending. The same households holding two unstable things together at once. When repossession comes, it doesn’t just wreck a credit score. It severs access to employment, childcare, basic functions in a metro area built around the assumption of a car. Job loss follows. Then rent default. Then eviction. The car is often the first domino, and nobody’s tracking it as such.

The median wealth of Black households nationally is roughly one-tenth that of white households — $24,520 versus $250,400, per Census Bureau data. There is no cushion. There is no soft landing. There is just a payment that is either made or not, with consequences that cascade immediately.

Minneapolis’s own Transportation Action Plan acknowledges this directly: over 30% of households of color in the city lack vehicle access, while transportation accounts for roughly 19% of household income. In some Minneapolis neighborhoods, 40-50% of households have no car at all. The people with the least access to cars are also the people most financially punished by the requirement to own one.

What That Money Could Otherwise Do

The $11,577 that a car costs each year isn’t just a big number. It is, dollar for dollar, the same argument that rent relief advocates have been making about housing for decades. Every dollar freed from transportation burden is a dollar available for stability — for emergency savings, for consistent rent, for the child care that makes a second income possible, for the small investment that compounds into something. At the neighborhood level, money that stays local instead of flowing to automakers, lenders, and oil companies builds the kind of economic resilience that tenant organizers are also trying to build. The transportation conversation and the housing conversation are after the same thing. They just haven’t figured that out yet.

Put it another way: $11,577 is nearly a full year of groceries for a family of four on the USDA low-cost food plan. It’s two years of community college tuition at Hennepin Tech or Saint Paul College. It’s the down payment on a house in North Minneapolis or Frogtown — the kind of wealth-building asset that actually appreciates, that can be passed to children, that doesn’t lose 20% of its value the moment you drive it off the lot. It is, in short, exactly the kind of capital that separates households that build equity over a generation from households that tread water. The difference between a car-dependent family and a transit-connected one isn’t just the monthly payment. It’s compounded, year over year, into the gap between owning something and owing something.

Instead, that money leaves. It flows upward. And low-income households pay the highest effective rate for this extraction, both because they carry more debt relative to income and because the lending market charges them more for the privilege.

The Policy Gap

Here is what the rent-relief framework gets right: housing is a social good requiring public investment. No family should face homelessness because of an economic shock they didn’t cause. That principle has enough political traction to produce emergency moratoriums, rental assistance programs, and years of organized advocacy.

The transportation equivalent of that principle barely exists as a political idea. Auto loan forbearance during a documented income emergency? Not a bill anyone’s running. Emergency relief for households whose transportation costs are consuming 38% of their take-home pay? Not a line in any budget. A moratorium on vehicle repossession when the community is mid-economic-crisis? Not a conversation happening at the Capitol.

This matters because the policy tools exist. We demanded forbearance from mortgage servicers in 2008. We demanded it from landlords in 2020. The Minnesota Department of Commerce has regulatory authority over financial institutions operating in this state. The argument for exempting auto lenders from the same expectations we applied to everyone else in a crisis doesn’t hold. It just hasn’t been made, because transportation burden isn’t yet a political coalition with real power behind it. The evidence is in the budget: as Bill Lindeke recently noted in MinnPost, the Governor’s supplemental budget — released while gas prices surge and immigrant workers across the state absorb the worst income disruption in a generation — contains exactly one significant transit line item. It’s a cut.

Tenant advocates and housing organizers should consider whether the coalition they’ve built belongs at this table. The families they’re already working with are the same families most at risk of losing their cars. The eviction they’re trying to prevent is downstream of the repossession they haven’t started tracking yet.

A Third of Us Were Never Going to Own That Car

One-third of Americans — roughly 110 million people — don’t have a driver’s license. Disability rights advocate Anna Zivarts lays out who they are in When Driving Is Not an Option: disabled people, lower-income people, formerly incarcerated people, undocumented immigrants, children, the elderly. A constituency the transportation system has rendered largely invisible, because it was designed by and for people who drive.

This is also, almost exactly, the population that the rent-relief conversation is already trying to reach.

Zivarts argues that when you design transportation around involuntary non-drivers instead of treating them as edge cases, the whole system gets better. More frequent buses help the person with no other option and the commuter who’d rather not drive. Safe sidewalks and protected bikeways serve the commuter who can’t afford a car and the parent running errands between bus stops. The crises unfolding right now — and in Part 2, we’ll get into exactly how bad they’ve gotten — are an argument for transit and active transportation as emergency resilience infrastructure. They’re also an argument for both as basic justice, owed to the third of the population who were never going to have that car, and to the growing number who are about to lose theirs.

Before We Can Get to Solutions

Most people who own a car in this region didn’t weigh the options and pick driving. They looked at when their shift starts, where the bus goes, how far the grocery store is, and whether their kid’s school is on any route that gets them there on time — and they did the math that the built environment did for them. The car wasn’t a choice so much as a conclusion.

For urbanists and multimodalists who have the good fortune to live near frequent transit or within biking distance of work, that’s worth sitting with. The freedom to opt out of car ownership is itself a product of where you can afford to live and what your job allows. It is not a virtue. The person commuting on I-35 at 5 a.m. isn’t failing to imagine a better world. They’re getting their kids to school and their body to work with the infrastructure that exists, the same as the rest of us.

The constituency that needs better transportation in this state isn’t drivers versus bus riders or versus cyclists. It’s everyone who is one car repair, one repossession, one income shock away from losing the only connection they have between where they live and where they need to be. That’s a very large group of people. It includes almost everyone this article has been about. Building toward something that works for them is the whole point—not as a political strategy, but because they’re our neighbors and they deserved better infrastructure long before any of this started.

In Part 2: How Operation Metro Surge detonated the auto loan bubble, why the second wave in greater Minnesota will hit harder, and what it means that the drawdown from Minneapolis relocated the crisis to places where there is no transit floor at all.